Any stage, any age, any wage!

Knowing when to invest, how to invest, and what to invest at any stage can be tricky. Every individual has different needs and goals, which has a huge impact on personal savings plan. We asked our branch staff at our Town Centre Branch asking for their investing advice for any stage, any age, and any wage and here’s what they came up with.

Investing in your 20’s and 30’s:

Emergency savings are key – ensuring you have savings for an unexpected expense like a car breakdown, job loss, health problems, or a sick relative or pet is crucial. The Financial Consumer Agency recommends saving up the equivalent of 3 to 6 months of regular expenses or 3 to 6 months of income. Saving gradually will help make seemingly impossible goals seem more realistic.

- At $5 a week, you’ll save $260 after one year

- At $10 a week, you’ll save $520 after one year

- At $15 a week, you’ll save $780 after one year

- At $20 a week, you’ll save $1,040 after one year

Other tips for investing in your 20’s and 30’s include setting clear goals – think about where you want to be financially in five to ten years, set a realistic goals, and stick to them. Not sure what a realistic goals looks like – have a chat with one of our financial planners; these trained advisors are helpful whether you have $1 or $100,000.

Finally, savings might not be at the forefront in your early years – taking advantage of any employer based savings plan such as a pension will help you out in the long run.

Setting up and contributing to your own RSP can prove beneficial for more than just retirement. It can help offset income tax, and you may be able to use some of your own RSP savings for a down payment on your first home, even use these savings to help fund additional education under the lifelong learning plan. Should you decide to borrow from your RSP for either of these programs, the funds will need to be repaid over a manageable period of time.

Investing in your 40’s:

In your 40’s, you often owe more money than you will in your 20’s, 30’s, 50’s… you get the picture. Likely, debt reduction will be a primary focus and this may have an impact on your personal savings. Whether you’re focused on paying down debt or saving for your child’s education, one thing was certain from our financial experts – don’t forget about yourself!

Contributing to a retirement savings plan can help offset income tax; and of course it will add to the amount of money you have saved for retirement. The money you allocate to pay down debt are extra dollars you will have freed up in your 50’s & 60’s. Be sure to talk to one of our financial advisors to help strategize the best path for your future financial goals.

Investing in your 50’s:

If you’re in your 50’s you’ve reached that milestone age – retirement and the end of your working years are within reach. You may find yourself making up for lost time if investing wasn’t a focus in your 20’s, 30’s, and 40’s. By 50, you should have 6 times your salary saved; if you make $60,000 per year, you should have a minimum of$360,000 in savings. This of course changes for every individual – if you’ve paid off your home, this will free up a significant amount of income in your retirement years.

The biggest take away from investing in your 50’s is that if you haven’t yet started investing, it’s not too late – start now and keep putting money aside each month. Celebrate the fact that you are investing, despite what the balance may look like – getting into that routine behaviour is what matters most. Play around with calculators on the internet and be sure to talk with your financial advisor about your financial goals. There is nothing worse for us than having to tell someone they are not able to retire because they don’t have enough money saved.

The power of compound interest!

One of the biggest reasons we promote investing in your early years is due to the power of compound interest. Compound interest can be a huge benefit to your investments because it allows you to receive interest on your interest.

For example:

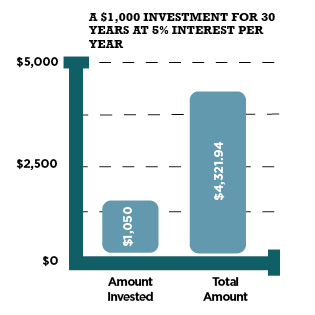

Say you invest $1,000 at an interest rate of 5% and your interest is paid annually. In the first year, you will receive $50 in interest; when you compound that interest, you allow the interest to be added to the principle amount of your investment, and the following year you are earning interest on $1,050. When interest is paid the following year, it is paid on the original $1,000, plus the $50 in interest, earning you an additional $52.50 in interest. If, over time, you never added any additional funds to this investment and continued to allow your interest to be added to your initial investment of $1,000, after 30 years, with a consistent rate of 5%, your investment of $1,000 would become $4,321.94.

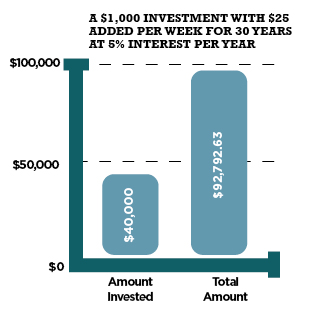

Now, this might not seem like a lot of money – but remember that this does not include any contributions. If you were to add $25 per week to this investment and consistently earn 5% in interest, compounding of course, your investment would be worth $92,792.63 after 30 years. So how much out of your pocket would you have to spend in order to earn this sum? $1,000 plus $25 per week for 30 years is only $40,000.

The moral of the story is if you make investing a priority and start in your early years, your investments have the potential to significantly impact your retirement savings.

Did you know that compound interest can also work against you?

When you owe money, compound interest can make it challenging to get ahead. Credit cards and lines of credit are a great example of compounding interest that works against you when you owe money. $5,000 on a credit card at an interest rate of 19.99% could take years to pay off only making the minimum payment and you could pay thousands of dollars in interest. You could end up paying almost twice as much as you owe by the time credit card debts are paid off.

Investing for your future and developing financial goals is an important element to getting older. Be sure to continuously review your investment goals, make a plan, make a budget, use online calculators to see where you’re at and where you should be, talk to our advisors for strategies and plans on the best course of action to take, and don’t forget that we are here to help. We’re here to enrich the lives of all we serve, using the full slate of innovative solutions in our toolbox.

So, any stage, any age, any wage – pop on by and chat with us about your financial future, or book an appointment. Your future self will thank you later.